Navigating the world of credit scores can be akin to mastering a financial high-wire act – it’s a balancing performance where every move can either keep you buoyantly afloat or send you into a free-fall. As you gingerly step towards your goal of credit score excellence, one misstep often overlooked is how credit card activities around your closing date can sway your score. Don those financial spectacles and let’s delve into the nitty-gritty of closing date credit card impacts on your all-important credit score.

Understanding the Impact of Closing Date Credit Card Activities on Credit Scores

Deciphering the Closing Date Credit Card Concept

Credit cards don’t just provide the convenience of cashless transactions; they’re a cog in the mechanism of your financial reputation. Picture this: your credit card statement cycle is like a month-long financial performance, and the closing date – the final act. After the curtain call on this date, your statement is generated, outlining the tale of your spending and payments. Notably, the transactions within this performance window are the ones spotlighted in the credit score script.

The Anatomy of a Credit Score: Where Closing Date Fits

A credit score is much like a gourmet dish – made up of various ingredients that must harmoniously blend together. Components such as payment history, debt levels, the age of credit history, mix of accounts, and new credit inquiries create this financial delicacy. But here’s the kicker – activities around the closing date can add a dash of zest or a spoonful of bitterness to your credit utilization, a key ingredient contributing to about 30% of your FICO score spice mix.

The Nuances of Credit Utilization and Closing Date Credit Card Balances

Balancing Act: Credit Utilization Ratios Explained

The credit utilization rate, a critical pivot point in credit scoring, is simply the portion of your credit limit you’re currently using. And, darling readers, the magic number to aim for is below 30%. Just like keeping a Louis Vuitton bag in pristine condition,^1 maintaining this optimal rate requires care.

Reporting Schedules: How Credit Card Companies Report to Bureaus

Each card issuer has their own rhythm, like seasons changing, with some reporting at the closing date while others pick a different time. This reporting date can dramatically influence your score just as the winter solstice heralds new beginnings.^2

| ITEM | DESCRIPTION |

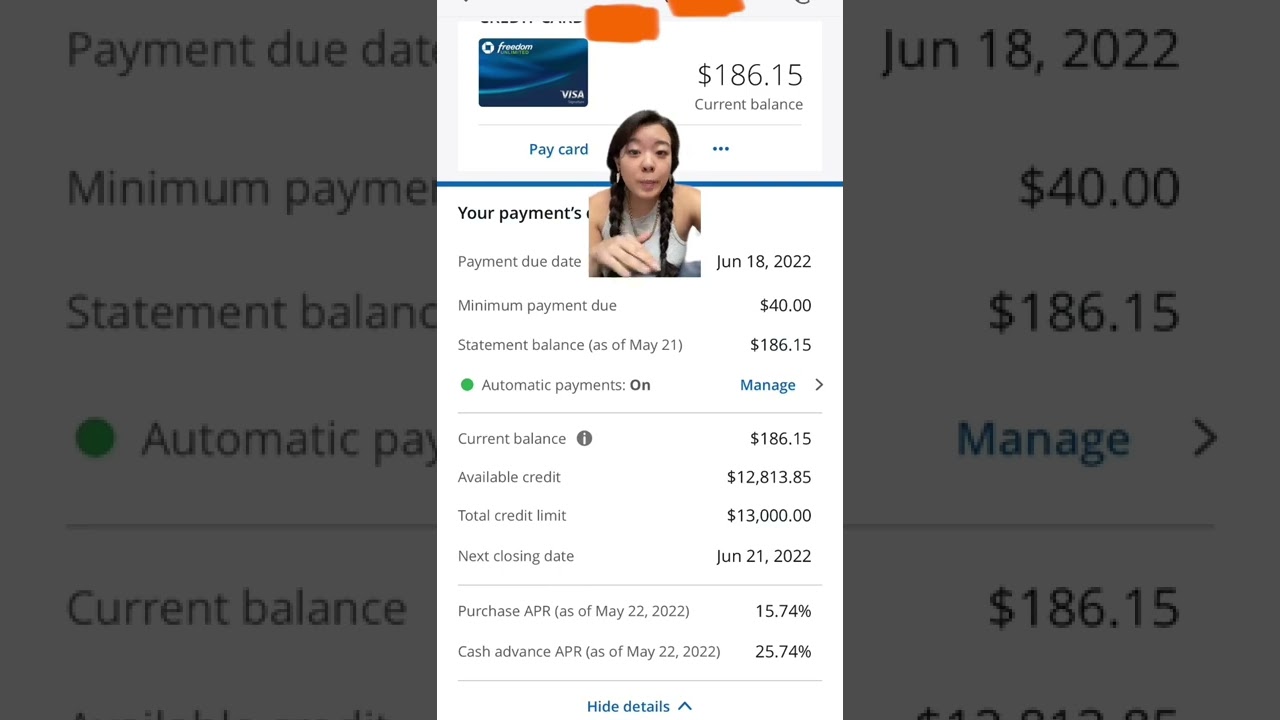

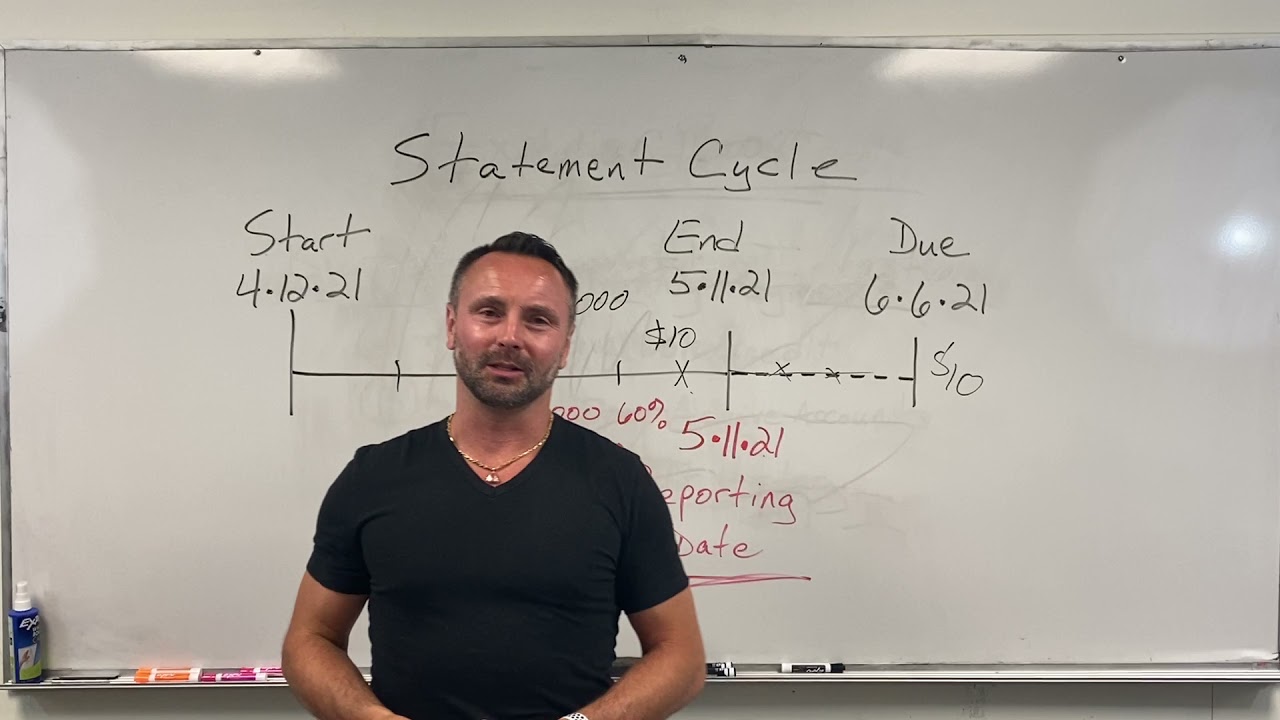

| Closing Date | The last day of your credit card billing cycle. On this date, your credit card statement is generated. |

| Statement Issue Date | This is the same as the closing date. Your statement is sent out detailing the transactions of the past billing cycle. |

| Due Date | At least 21 days after your closing date, this is the deadline to make at least the minimum payment to avoid late fees and interest. |

| Payment Strategy | To minimize interest and boost credit score, pay down the balance before the closing date, especially if the debt-to-credit ratio is high. |

| Charges Between Due Date and Closing Date | These will appear on the following billing statement and are not due until the next cycle’s due date. |

| Minimum Payment | The smallest amount you can pay by the due date to keep the account in good standing, though paying only the minimum can result in significant interest charges. |

| Late Fees and Interest | Failing to pay at least the minimum by the due date can lead to these additional costs. |

| Consequences of Closing a Credit Card | May negatively impact your credit score due to changes in credit utilization and history length. |

| Credit Utilization | Keeping credit card balances low relative to the credit limit is preferable for a good credit score. |

| Advice from Expert (Beverly Harzog) | It’s advised not to close credit cards even if they are unused, as it can potentially decrease your credit score. |

Closing Date Credit Card Payments: Timing is Everything

The Ripple Effect of Early vs. On-time Payments around the Closing Date

Imagine the credit card payment as Cybill Shepherd made a dramatic entrance in a scene – timing is crucial.^3 Early payments, before the closing date, could mean a grand debut for your credit score; on-time payments ensure it stays consistent.

The Hidden Challenges of Late Payments Close to the Closing Date

If late payments are the villains in our story, then making one right before the closing date is downright diabolical. Think Ed Norton delivering a knockout performance – it’s impactful and lasting.^4

Credit Score Myth-Busting: Does Closing a Credit Card Hurt Your Score?

Closing Credit Card Accounts: Knowing the Facts from the Myths

It’s the cliffhanger at the end of season one — does closing a credit card account really hurt your score? “And just like that,” the answer is nuanced.^5 The true impact depends on your credit history and current balances.

Strategies for Gracefully Closing Credit Card Accounts

Should you decide to bid adieu to a credit card, timing is again, your co-star. Closing an account immediately after a closing date allows for a final financial bow on good terms.

The Long-Term Perspective: Closing Date Credit Card Habits for Score Improvement

The Science of Habit Formation and Credit Card Use

Kevin Doyle once said that habits carve out our financial future like a river shapes a canyon.^6 Developing positive habits in line with closing dates can create a stunning landscape for your credit score to flourish.

Real-Life Success Stories: Closing Date Credit Card Management

It’s the rags to riches storyline; individuals who have fine-tuned their spending and payments in alignment with the closing date witness a gradual but significant escalation in their credit scores.

Navigating Credit Card Closures with an Eye Towards Future Goals

The Role of Closing Date Credit Card Decisions in Financial Planning

Each move you make with your credit card leading up to the closing date could be setting the stage for the grand drama of getting a mortgage with favorable interest rates.

Credit Card Closing Date Tactics for Proactive Credit Health

Proactive is the key term here – aligning credit card activities pre-closing date just like you would align your energies for achieving an overarching goal.

The Art of Credit Card Balance and Closing Date Synergy

Merging Credit Card Balance Management with Closing Date Awareness

The tango between your balance management and the closing date necessitates grace and awareness. With the right strategy, you’ll never miss a beat.

Crafting a Bright Credit Future: Innovative Strategies Beyond the Closing Date

Beyond the Numbers: Embracing a Holistic Approach to Credit Health

The journey to stellar credit health extends beyond mere numbers to include education, diligence, and a dash of foresight. Remember, knowledge is power, and understanding the ebb and flow of closing dates keeps you ahead of the game.

The Horizon of Credit Score Enhancement: Emerging Trends and Insights

As trends shift like sand dunes, it pays to be on the cutting-edge of credit score innovation. Stay alert for new twists in the credit landscape, be adaptable and ready to pivot your strategy as needed.

Envisioning a Credit-Savvy Future: Key Takeaways for Closing Date Credit Card Mastery

Reflecting back on our journey, let’s reiterate a few cardinal rules for conquering the credit score arena:

Hear me out when I say, dear readers, that with persistence, deliberation, and a touch of finesse, you’ll not only master the act of closing date credit card harmony but also pirouette into a future where you’re not just surviving the financial tightrope, but expertly performing to standing ovations. Let the show begin!

How Your Closing Date Credit Card Magic Works

Hold your horses, because we’re about to unveil some must-know gems about that magical moment known as your credit card’s closing date. It’s like the grand finale of your card’s billing cycle, where the curtains close, and the spotlight shines on your spending masterpiece. But before we dive into the nitty-gritty, let’s get comfy with a few fun-sized facts and tidbits that might just tickle your financial fancy.

The Final Countdown: Understanding Your “Closing Date”

Alright, gather ’round! You know that feeling when you’re at the end of a “billing cycle”, and the anticipation is killing you? Yup, that’s your credit card’s closing date playing hard to get. It’s the date when your lender takes a snapshot of your account; think of it as a financial selfie that shows off everything you’ve bought, from those snazzy sneakers to the late-night pizza runs.

The Sneaky Impact on Your Credit Score

Now, don’t let it catch you off-guard, but this charming closing date on your credit card is quite the influencer. It’s got the power to send your credit score swinging like a pendulum! Pay close attention, and you might just catch it whispering sweet nothings to the credit bureaus, telling tales of your spending habits.

Say What? Your Payment Isn’t Due Yet?

Hold the phone! Just when you thought you had it all figured out, here’s a little twist – your payment isn’t even due on the closing date! Nah, your lender gives you this grace period, a time where you can chill out before you have to shuffle over your hard-earned dough.

Pro Tips to Keep Your Scores Soaring

Alright, buddy, lean in close for the pro tip of the century – timing is everything. If you’re smart about it, and treat your closing date with the respect it deserves, you’re on the pathway to credit score paradise.

So, what’s the big secret? Pay your dues before the closing date, and your credit report will make you look like a financial angel, halo and all. No kidding! Doing this can make your balance seem lower when the credit bureaus take a peek at your financial snapshot. And hey, who doesn’t like looking extra savvy in their financial selfie?

Ready for the Encore?

Well, don’t just sit there! With these sparkly bits of trivia tucked into your brain pocket, you’re all set for navigating the intriguing world of credit cards. And remember, the closing date credit card dance is one you want to get right – it could be the difference between a standing ovation and getting tomatoes thrown your financial stage.

Have fun out there, but keep your wits about you. It’s a financial jungle, and now, you’re ready to swing from the credit vines like a pro.

Should I pay off my credit card before the closing date?

Oh, absolutely! Knocking out your credit card balance before the closing date is a smart move. It’ll not only give you a tidy balance of zero but also show credit bureaus you’re on top of your game, which could give your credit score a nice little boost. Who wouldn’t want that?

What does closing date mean?

“Closing date” – don’t let the term throw you for a loop. It’s just the end of your credit card billing cycle, and, spoiler alert: it’s when your statement gets generated. This is the date up until which all your purchases get tallied up to be paid by the due date. Simple, right?

Is it better to let a credit card expire or close it?

Here’s the skinny: letting a credit card expire might seem like the easy road, but it could leave a ding on your credit score. If it’s adios amigo, it’s better to officially close it to avoid any nasty surprises. Plus, you’ll keep your credit history cleaner than a whistle!

Can I use my card after the closing date?

Yesiree, you can keep swiping that plastic even after the closing date. But remember, every new charge will show up on the next statement, so keep a lid on the spending, okay?

What is the 15 3 rule for credit cards?

The 15/3 credit card rule isn’t rocket science, folks. Paying a chunk of what you owe 15 days before the closing date, and then the rest 3 days before, can play nice with your credit utilization and potentially keep your credit score jumping for joy.

Is it bad to pay your credit card bill multiple times a month?

Not at all! Paying off your credit card multiple times a month can actually be a pretty slick move. It shows you’re on the ball and can keep your credit utilization lower than a snake’s belly. Win-win!

Why is closing date important?

The closing date’s like the grand finale of your billing cycle – super-duper important. It decides which purchases make it onto which statement, and it signals when your credit use gets reported. Keep your eyes peeled so you’re not caught on the back foot!

What is the difference between payment and closing date?

Okay, think of it this way: the payment date is when you fork over the cash to cover your charges, while the closing date is when they call time on your billing cycle and tally up what you owe. It’s like the referee blowing the whistle at the end of the game!

Does closing date mean last day?

Aha! The closing date does indeed mark the tail end of your billing cycle. But don’t get it twisted – it’s not like Cinderella’s coach turning back into a pumpkin; you’ve still got time before you have to pay up by the due date.

Is it bad to close a credit card with zero balance?

Closing a credit card with a zero balance? It’s not the worst thing, but keep in mind, it might put a dent in your credit score, especially if it’s an older card. Like saying goodbye to an old friend, sometimes it’s necessary, but make sure it’s the right move for your wallet.

Is it bad to have a lot of credit cards with zero balance?

Hold your horses! A bunch of cards with a zero balance might not be bad, but it’s kinda like walking a tightrope. Lenders might wonder why you need all that credit. Just keep it balanced, and you’ll stay on the straight and narrow.

Is it bad for your credit to let a credit card close?

Letting a credit card close on you, especially if it’s from inactivity, can be a bit of a no-no. It’s like accidentally letting go of a balloon – up goes your credit utilization, and there goes your credit score.

Are payments made on closing date?

Payments made on the closing date can be like sliding into home base just as the catcher gets the ball. If the timing is perfect, it’ll count for that billing cycle. But careful, timing is everything, and a day late could mean waiting another whole cycle.

When should I pay my credit card bill to increase credit score?

Hitting the sweet spot when paying your credit card bill is golden for boosting your credit score. Aim to pay before the statement date to lower your utilization, and let me tell you, your credit score will be happier than a clam at high tide!

Can I pay my credit card early and use it again?

You betcha! Paying your credit card early is playing it savvy, and then, guess what? You can totally go for another round with your card – just make sure your spending’s on track, and you’re not putting yourself in a tight spot.

Can I make a payment on the closing date?

It’s last-minute, but making a payment on the closing date can still count. If the stars align and the payment goes through on time, it’ll be like you scored a three-pointer at the buzzer – in the nick of time!

What happens if I make a purchase on my closing date?

Here’s the deal with a purchase on the closing date: it’s like a buzzer-beater in basketball. If it gets processed in time, it slides into your current billing cycle. If it doesn’t, it’s on deck for the next one. Keep a watchful eye!

How long after closing is the first payment due?

After closing the deal on your home, the first mortgage payment usually hits the stage about a month after the next month starts. So if you close in April, you’re looking at a due date around June 1st – give or take a few days for grace periods. Mark those calendars!

Do you have to close by closing date?

Well, you don’t have to close by the closing date, but it’s not a bad idea to aim for it. It’s a lot like hitting a deadline – you can breathe easy when it’s done, avoid the nail-biting, and dodge any extra fees or complications. Whew!