Unveiling the Best Home Buying Calculator for Your Budget

In today’s digital era, one key tool stands out for prospective homeowners: the home buying calculator. Whether you’re a first-time buyer or looking to upsize, utilizing the right home buying calculator can significantly simplify your planning. This article delves into the top calculators available in 2024, ensuring you can make the best financial decisions for your situation.

The Importance of a Reliable Home Buying Calculator

Investing in real estate is no small feat. A reliable home buying calculator helps demystify the process, providing clear insights into what you can afford, hidden costs, and potential mortgage plans. Here, we discuss why using a high-quality home buying calculator is essential for your future home purchase.

Firstly, buying a home involves numerous variables: down payments, interest rates, taxes, insurance, and more. A solid home buying calculator brings all these elements together, offering a comprehensive view of your financial preparedness. Secondly, these tools help in planning by simulating different scenarios, showing how potential changes in your income or expenses could impact your buying power. Lastly, good calculators include features such as amortization tables and loan comparisons, which are invaluable for long-term financial planning.

With a reliable home buying calculator, you gain a clearer picture of your financial boundaries and opportunities, enabling smarter, more informed decisions. This is crucial whether you’re buying your first home or looking to invest in a new property.

| Income Level | Affordable Home Price Range | Corresponding Monthly Payment | Assumptions |

| $70,000/year | $290,000 – $310,000 | $2,000 – $2,500 | Includes monthly mortgage, taxes, and home insurance. |

| $93,438.60/year | $400,000 | $2,495.52 | 20% down payment, 6.5% interest rate, 30-year mortgage, $1,000 in monthly debt. Gross monthly income needed: $7,786.55. |

| $36,000/year | $100,000 – $110,000 | Just over $1,000 | Assumes no other debts and minimal savings for down payment. |

| General Rule | Housing expenses should be <28% of monthly gross income. Housing + other debts should be <36% of monthly gross income. |

Top 7 Home Buying Calculators in 2024

In this section, we’ll explore the crème de la crème of home buying calculators, considering factors like user interface, accuracy, and additional features.

How to Choose the Right Home Buying Calculator

Selecting the best home buying calculator depends on your unique needs and financial situation. Consider the user interface, the depth of analysis provided, and any additional tools or insights relevant to your circumstances. Personalization is key—ensure the tool can adapt to your specific financial nuances.

When choosing the right home buying calculator, user-friendliness is paramount. A tool that’s easy to use will save you from possible headaches down the road. Also, look for calculators that offer detailed analyses, providing insights beyond basic payment estimations. Additional tools, such as those that offer credit improvement tips or investment advice, can be immensely beneficial.

Lastly, a good calculator should evolve with you, factoring in any future financial changes, like a job promotion or added expenses. Make sure you choose a calculator that not only meets your current needs but also adapts to your future financial landscape.

Maximizing the Benefits of Your Home Buying Calculator

To fully leverage these calculators, input accurate and current financial data. Consider potential changes in income or expenses and use the advanced features like amortization tables or loan comparisons to get a holistic view.

Inputting precise data ensures that your calculated figures reflect reality, letting you plan effectively without surprises. Furthermore, considering future income changes or additional expenses provides a cushion against unexpected financial shifts.

Utilize advanced features like amortization tables, which show how your mortgage payments will be distributed over time, and loan comparisons, which help identify the best financing options available. This thorough approach can provide clarity and confidence as you move forward in the home buying process.

Crafting Your Path to Homeownership

In the complex world of home buying, having a dependable calculator is akin to having a seasoned guide. The right tool empowers you to chart the financial territory with confidence and make choices that align with your future aspirations. Dive deep, explore these calculators, and take the first step towards securing your dream home in 2024. For instance, if you’re making $70K a year, you’re likely looking at homes between $290,000 and $310,000 with monthly payments ranging from $2,000 to $2,500. This is where a comprehensive home calculator comes in handy.

Whether you find yourself intrigued by properties with character, like those owned by the escape From new york cast, or you’re more into practical investments like an Adidas superstar Mens collection, getting the right financial tools means you’re always one step ahead. Start with exploring these top calculators, like the ones on Mortgage Rater and home finance Calculators, to make well-informed decisions.

Use your home buying calculator, consider every angle, and make the complex decisions that will help you secure your future. After all, nothing beats the feeling of turning the key in the door of your dream home. No matter your situation, a reliable home buying calculator is your trusty sidekick on this adventure, offering support, insight, and clarity every step of the way.

Fascinating Facts About Your Home Buying Calculator Experience

Buying a home is no small feat, but did you know that home buying calculators can make a huge difference? They’re often packed with surprises and fun facts that make the journey less daunting. Let’s dive in!

The Magic Behind the Math

When you think of home buying calculators, complex algorithms probably come to mind. But wait, there’s more! These tools were inspired by mathematical models used in varying fields. Believe it or not, even the precision used by ventriloquists like Terry Fator plays a part in the accuracy of financial simulations. You might not see the connection at first, but just as Terry mesmerizes audiences with his control, a home buying calculator orchestrates numbers to present clear, insightful results.

High-Tech and User-Friendly

Did you know that the development of home buying calculators parallels some creative innovations? The streamlined interfaces and intricate algorithms can draw a surprising parallel to cultivation techniques used in strains such as Jack Herer. As growers aim for the perfect balance in their strains, developers strive to build calculators that balance ease of use with robust functionality. The behind-the-scenes dedication ensures you get the best possible experience when calculating your future home expenses.

Pop Culture Meets Finance

Surprisingly, home buying calculators share cultural influences with areas you’d never expect! For instance, the engaging graphics and functional aesthetics might remind you of the vivid and detailed world in Kiddo from One Piece. This popular anime emphasizes the meticulous detail and seamless navigation appreciated by users of high-quality financial tools. The way each piece of the puzzle fits together shows the same attention to detail found in your go-to budget calculators.

Whether you’re crunching numbers or catching the latest trends, it’s clear that the humble home buying calculator is a product of innovation, creativity, and a dash of unexpected inspiration.

How much house can you buy if you make $70000 a year?

If you make $70K a year, you can probably afford a home priced between $290,000 and $310,000. This typically means your monthly house payment, which includes mortgage, taxes, and insurance, would range from $2,000 to $2,500.

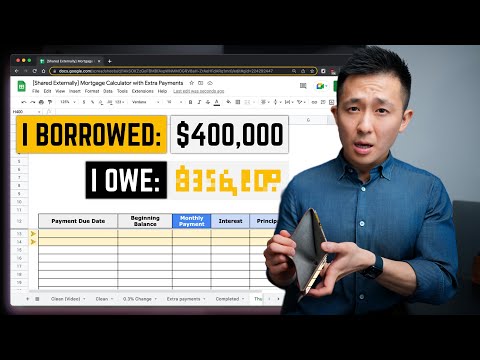

How much money do I need to make to buy a $400 000 house?

To afford a $400,000 home with a 20% down payment and a 6.5% interest rate on a 30-year mortgage, you’d need a gross monthly income of around $7,786.55, assuming you have $1,000 in monthly debt repayments.

How much house can I afford if I make $36,000 a year?

With a $36,000 annual salary, you can afford a house priced around $100,000 to $110,000. This assumes you have minimal or no debt and haven’t saved much for a down payment, resulting in a monthly payment just over $1,000.

How much house can I afford based on my salary?

Aim to keep your housing expenses below 28% of your monthly gross income. If you have other debts, both your housing expenses and debt payments should not exceed 36% of your monthly gross income. This approach can help you determine a comfortable purchase budget.

Can I afford a 300K house on a 60k salary?

If you make $60K a year, it’s a bit tight to afford a $300K house, but it might be possible depending on the interest rate and the size of the down payment. Ideally, your housing expenses shouldn’t stretch your budget too thin.

Can I afford a 200k house on a 70k salary?

With a $70K salary, you can comfortably afford a $200K home. Your monthly house payments, including mortgage, taxes, and insurance, would fit well within your income range.

How much income do I need for a $800000 house?

To buy an $800,000 house, you would need a substantial income. Depending on the down payment and interest rate, your annual income should be around $150,000 or more to comfortably manage the mortgage payments.

What is the 20% down payment on a $400 000 house?

For a $400,000 house, a 20% down payment would be $80,000. This reduces the upfront amount you need to borrow and can also lower your monthly mortgage payments.

What is the minimum income for a 300k mortgage?

For a $300K mortgage, you generally need an annual income of about $75,000 to $80,000. This ensures the monthly payments fit comfortably within the 28% threshold of your gross income.

Can a single person live on $36,000 a year?

Living on $36,000 a year as a single person is doable, but it requires careful budgeting. You’ll need to manage your expenses well to cover housing, utilities, food, transportation, and other essentials.

Can someone who makes 40k a year afford a house?

If you make $40K a year, affording a house is possible but will likely mean looking for homes in a lower price range, around $150,000. It also helps if you have minimal debt and possibly some savings for a down payment.

How much house for $3,500 a month?

With $3,500 a month to spend on housing, you could potentially afford a home priced around $400,000 to $450,000, depending on your down payment and other debts. This estimate includes all housing costs like mortgage, taxes, and insurance.

What is the ideal credit score to buy a house?

A credit score of 620 or higher is generally recommended to buy a house. Higher scores can help you secure better interest rates, which can lower your monthly payment and overall loan costs.

Will interest rates go down in 2024?

Predicting interest rate trends is tricky, but there’s hope they might go down in 2024 based on current economic indicators. Keeping an eye on economic news and consulting with a financial advisor can provide better guidance.

What is the 28/36 rule?

The 28/36 rule is a guideline to help manage your finances. It suggests that you spend no more than 28% of your gross monthly income on housing costs and no more than 36% on total debts, including your mortgage, car loans, and credit card payments.