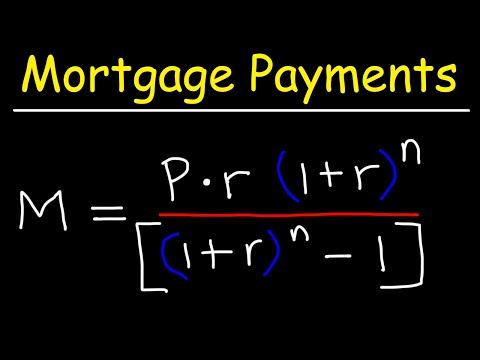

Understanding the Mortgage Monthly Payment Calculator: A Crucial Tool in Home Financing

A mortgage monthly payment calculator is an essential tool for potential homeowners and current mortgage holders alike. This invaluable resource allows borrowers to estimate their monthly mortgage payments accurately, taking into account various factors such as loan amount, interest rate, and loan term. Whether you’re eyeing a 15-year or 30-year loan, the calculator helps you gauge your monthly obligations. It’s especially handy when you’re trying to figure out how much you’ll owe on a $300,000 mortgage with a 6% APR, a $500K mortgage at a 7.1% interest rate, or even higher-priced homes.

Understanding these calculators streamlines your home financing process. You can arrive at a practical budget that includes your mortgage payment, taxes, insurance, and PMI (Private Mortgage Insurance). Essentially, these calculators aren’t just for math whizzes; they’re for anyone who wants to make informed financial decisions. So, if you’re wondering how much your monthly payments might be, let’s dive into some top mortgage monthly payment calculators.

Top Mortgage Monthly Payment Calculators in 2024

1. Bankrate Mortgage Calculator

Bankrate is a renowned name in the financial industry, making its mortgage calculator one of the most reliable options on the market. The user-friendly interface, coupled with comprehensive functionality, ensures that users can easily compute their monthly payments. Bankrate’s tool also allows for the inclusion of taxes, insurance, and PMI, offering a more holistic view of mortgage expenses.

Unique Features:

2. Mortgage Calculator by Zillow

Zillow’s mortgage calculator stands out for its integration with the real estate platform’s extensive property listings. This feature provides an immediate context for potential buyers, allowing them to estimate payments on homes they are interested in.

Unique Features:

3. NerdWallet Mortgage Calculator

NerdWallet offers a comprehensive mortgage monthly payment calculator designed for both novice and experienced homeowners. This tool provides robust educational resources that can help users understand the nuances of mortgage payments, interest rates, and loan terms.

Unique Features:

4. Quicken Loans Mortgage Calculator

As a major player in the mortgage lending industry, Quicken Loans offers a calculator that is seamlessly integrated with its loan application process. This tool is particularly useful for those who are already considering a mortgage with Quicken Loans.

Unique Features:

5. Chase Mortgage Calculator

Chase, a flagship banking institution, provides a sophisticated mortgage monthly payment calculator that not only estimates payments but also offers insights into loan eligibility.

Unique Features:

| Loan Amount | Interest Rate | Loan Term | Monthly Payment | Additional Information |

| $300,000 | 6.00% APR | 15 Years | $2,531.57 | Excludes escrow; escrow costs vary by location, insurer, etc. |

| $300,000 | 6.00% APR | 30 Years | $1,798.65 | Excludes escrow; escrow costs vary by location, insurer, etc. |

| $600,000 | 7.00% Fixed | 15 Years | $5,393.00 | Monthly payment only, escrow costs not included. |

| $600,000 | 7.00% Fixed | 30 Years | $3,992.00 | Monthly payment only, escrow costs not included. |

| $500,000 | 7.10% Fixed | 30 Years | $3,360.16 | Monthly payment can range from $2,600 to $4,900 depending on details. |

| ~$200,000 | Varies | Varies | ~$2,000 | Possible in over half the U.S. with $2,000 monthly budget, incl. taxes |

How to Choose the Best Mortgage Monthly Payment Calculator

Selecting the right mortgage monthly payment calculator depends on your specific needs and financial situation. Here are some key factors to consider:

User-Friendly Interface

A calculator that is intuitive and easy to use can save you time and effort. Tools like those offered by Zillow and Bankrate often get high marks for user experience.

Comprehensive Data Inputs

The best calculators allow you to input comprehensive data, including loan amount, interest rate, loan term, taxes, insurance, and PMI. Quicken Loans and Bankrate excel in this regard.

Real-Time Interest Rates

Access to updated interest rates ensures the accuracy of your monthly payment estimates. Tools from NerdWallet and Chase provide real-time data, which is invaluable for precise calculations.

Additional Features

Features like amortization schedules, side-by-side loan comparisons, and prequalification options can significantly enrich your planning process. Zillow and Quicken Loans offer particularly robust additional features.

Making the Most of Mortgage Monthly Payment Calculators

Scenario Analysis

Leverage these calculators to perform scenario analysis. For example, see how varying interest rates or loan terms impact your monthly payments. This helps in making informed decisions when negotiating loan terms with lenders.

Budget Forecasting

Use insights from your mortgage calculator to create a detailed budget forecast. Understanding your monthly obligations prepares you for potential financial challenges and ensures you maintain a healthy financial balance.

Educate Yourself

Don’t just use the calculator; take advantage of the educational resources that many of these platforms offer. Sites like NerdWallet and Bankrate provide extensive tutorials and articles that can deepen your understanding of mortgage-related finances.

Final Thoughts on Navigating Mortgage Monthly Payment Calculators

Mortgage monthly payment calculators are more than just tools; they’re crucial in making informed financial decisions regarding home finance. From understanding the impact of different loan terms to planning your long-term budget, these calculators can guide you every step of the way. By utilizing tools from trusted sources like Bankrate, Zillow, NerdWallet, Quicken Loans, and Chase, you can enter the mortgage process with confidence, ensuring your journey to homeownership is both manageable and well-informed.

For more insights and to use a comprehensive mortgage loan payment calculator, make sure to visit Mortgage Rater. Your journey to informed home financing starts here!

Discover Fascinating Insights with Our Mortgage Monthly Payment Calculator

Mortgage Monthly Payment Calculator: A Wealth of Knowledge

Did you know that using a mortgage monthly payment calculator not only saves time but can also unveil some intriguing facts about home loans? These tools demystify the financial jargon, allowing you to grasp the nuances of home financing. For example, the mortgage Loans calculator includes features that help you break down your loan payments effortlessly. Talk about hitting the nail on the head, right?

These calculators often employ the compound interest formula interest to show how interest accumulates over time. It’s wild to think about how compound interest can significantly impact the total amount you’ll pay. However, the flip side is that understanding this can help you make smarter financial decisions. It’s not merely about crunching numbers but making informed choices.

Trivia Nuggets to Ponder

Here’s a fun nugget: Your mortgage monthly payment calculator can sometimes feel like a treasure hunt! You might think you’re just inputting numbers, but occasionally, it leads to surprising revelations, like finding hidden savings much like discovering unclaimed money in Maryland. Imagine finding out you’re eligible for a lower interest rate or a shorter loan term than you initially expected. Eureka moments like these make the mundane task of financial planning a bit more exciting.

For those who enjoy a bit of history, did you know that Lee Malvo, infamous for his criminal activities, had a significant impact on communities, indirectly affecting real estate markets and loan rates? The ripples from such events can sometimes be seen in tools designed to help you understand today ‘s mortgage rates. Society’s ebbs and flows often influence the financial tools at our disposal.

Maximize Your Savings

One of the most compelling reasons to use a mortgage monthly payment calculator is the clarity it provides on overall loan repayment. Tools like the mortgage payback calculator can be revealing, allowing you to see the full picture of what you’ll pay over the life of the loan. Such insights can prevent you from getting a nasty shock down the road and help plan for a comfortable financial future.

Even if anime isn’t your thing, you might be amused to know that even an anime butt could metaphorically help teach lessons in financial amortization. Just as animation can bring complex characters to life, a mortgage calculator animates your payment schedule to help you see where every penny is going. It creates a visual representation of a financial journey that might otherwise be hard to grasp.

So, when you’re ready to dive into home financing, let a mortgage monthly payment calculator be your go-to tool for revealing the less obvious yet important aspects of your mortgage. It’s like having a knowledgeable friend by your side, guiding you towards a better financial future.

How much does a $300 000 mortgage cost per month?

On a mortgage of $300,000 with a 6% APR, you would be looking at paying $2,531.57 per month if it’s a 15-year loan and $1,798.65 per month if it’s a 30-year loan. Keep in mind, this doesn’t include escrow costs, which can vary.

What is the monthly payment on a $600000 mortgage?

For a $600,000 mortgage at a 7.00% fixed interest rate, you might expect to pay around $3,992 a month on a 30-year mortgage, while a 15-year plan could bump it up to about $5,393 a month.

How much is a 500K mortgage monthly?

With a $500,000 mortgage over 30 years at a 7.1% interest rate, your monthly payment would be around $3,360.16. However, it can fluctuate between $2,600 and $4,900 depending on the term and rate specifics.

Is $2000 a month a lot for mortgage?

A $2,000 monthly mortgage is quite common in many parts of the country. In fact, you could afford a house within this budget in more than half the states, considering property taxes and other factors.

Can I afford a 300K house on a 60k salary?

On a $60,000 salary, affording a $300,000 house might be tight. Mortgage lenders typically recommend that your monthly mortgage payment should be no more than 28-30% of your gross monthly income, so the numbers might not favor a $300K home on $60K.

How much house can I afford if I make $70,000 a year?

Making $70,000 a year, you might afford a home in the range of $280,000 to $330,000, assuming you follow the common advice that suggests spending around 4 to 4.7 times your income on a property.

How much house can I afford if I make $36,000 a year?

If you earn $36,000 annually, your house affordability might hover around $144,000, give or take some, considering you’d want to keep your mortgage payments reasonable and within recommended guidelines.

How much income do you need for a $500 000 mortgage?

To comfortably carry a $500,000 mortgage, you’d generally need an annual income in the ballpark of $125,000 or more, following the typical debt-to-income ratios lenders look at.

How do people afford a $600000 house?

Affording a $600,000 house often means having a solid income, usually over the $150,000 mark, along with managing existing debt, having a good credit score, and saving for a sizeable down payment.

How much is a 20 down payment on a 500 000 house?

A 20% down payment on a $500,000 house would be $100,000. It’s a significant amount, but it helps in cutting down your monthly mortgage payments and possibly avoiding private mortgage insurance (PMI).

Will interest rates go down in 2024?

Predicting interest rates isn’t an exact science, but some experts believe there might be a slight decrease in 2024. Keep an eye on economic trends and Federal Reserve announcements for better insight.

How much do you need to make to afford a 550K mortgage?

For a $550,000 mortgage, you’d generally need to pull in around $137,000 per year to meet the standard lending criteria comfortably.

Is 40% of income on a mortgage too much?

Spending 40% of your income on a mortgage can be pretty heavy and might leave you thinly spread with other expenses, saving goals, and emergency funds.

Is 50% of take home pay too much for a mortgage?

Dedicating 50% of your take-home pay to a mortgage can be risky and isn’t typically advisable. Most financial experts suggest keeping it under 30% to maintain a healthy financial balance.

What is the 28 36 rule?

The 28/36 rule suggests you should spend no more than 28% of your gross monthly income on housing expenses and no more than 36% on total debt payments. It’s a guideline to help maintain financial health.