When exploring the ins and outs of mortgage financing, one tool that rises to the top in 2024 is the total mortgage cost calculator. It’s an indispensable asset for homebuyers who hope to fully comprehend their entire mortgage expenses—not merely the monthly payment.

Understanding the Total Mortgage Cost Calculator

How Total Mortgage Cost Calculators Work

Total mortgage cost calculators account for various elements that contribute to the total expense of a mortgage. These elements include principal and interest payments, property taxes, homeowner’s insurance, private mortgage insurance (PMI), and sometimes homeowners association (HOA) fees. They aggregate these costs, offering a holistic view beyond the simplistic monthly mortgage payment.

Top 5 Total Mortgage Cost Calculators of 2024

1. Bankrate’s Total Mortgage Cost Calculator

Bankrate’s total mortgage cost calculator is a gem for comprehensive financial planning. Their calculator provides an all-encompassing breakdown of costs over the life of the loan, giving users detailed insights into every financial aspect involved.

Features:

– Customization: Allows users to adjust variables such as loan term, interest rate, and property value, offering a personalized estimate.

– Detailed Explanation: Provides in-depth analysis of how each factor affects the total cost.

– User-Friendly Interface: Simplifies navigation for both seasoned and first-time homebuyers.

2. NerdWallet’s Total Mortgage Cost Calculator

NerdWallet’s calculator is praised for its user-centric experience. Intuitive and easy-to-navigate, it’s ideal for users who desire quick yet comprehensive insights.

Features:

– Interactive Charts: Offers visual representations to easily compare different mortgage scenarios.

– Comprehensive Breakdown: Details fees, interest over the loan’s lifespan, and potential PMI.

– Customizable Inputs: Updates immediately as users adjust input variables.

3. Zillow’s Total Mortgage Cost Calculator

Zillow excels with its localized and personalized estimates. By tapping into its extensive database, Zillow can provide nuanced projections based on specific property details.

Features:

– Local Data Integration: Uses accurate property taxes and insurance estimates based on location.

– Interactive Sliders: Eases tweaking of mortgage amounts, interest rates, loan terms, and down payments.

– Comparison Tool: Evaluates various loan programs and their long-term costs.

4. SmartAsset’s Mortgage Calculator

SmartAsset’s mortgage cost calculator is revered for its depth and flexibility. It’s excellent for those wanting to dive deeper into different financial scenarios.

Features:

– Scenario Analysis: Enables side-by-side comparisons of different mortgage options.

– Refinancing Options: Includes potential refinancing scenarios and their future impact.

– Financial Guidance: Offers actionable advice based on the calculated data.

5. Freddie Mac’s Total Mortgage Cost Calculator

Freddie Mac’s tool is a powerhouse, especially for those aiming for data-rich insights from a trusted financial institution.

Features:

– Detailed Reporting: Offers comprehensive reports on total mortgage costs, including amortization schedules.

– User Guidance: Provides extensive tips and guidelines to help new buyers understand complex financial terms.

– Realistic Estimates: Utilizes current market data for accurate cost projections.

| Category | Details |

| Loan Amount | $500,000 |

| Interest Rate | 7.1% |

| Loan Term | 30 years |

| Monthly Payments | $3,360.16 |

| Annual Payments | $40,321.92 |

| Total Payments | 360 (30 years x 12 months per year) |

| Total Interest | Calculated monthly interest * number of months |

| Interest Charges | For the life of the loan, add up all monthly interest payments |

| Loan Fees | Combined interest charges + any applicable loan fees |

| Calculation of Monthly Cost | \[($500,000 x 0.071) / 12] to get monthly interest, and then add principal portion of monthly payment |

| Example Cost Breakdown (Yearly) | $500,000 mortgage with 7.1% interest rate: $3,360.16 monthly x 12 = $40,321.92/year |

| Formula for Total Payments | Loan Term (years) x 12 (months/year) e.g., 30 years x 12 = 360 payments |

| Key Features | Estimates total mortgage costs over the life of a loan; includes interest and potential loan fees |

| Benefits | Helps borrowers understand lifetime mortgage costs; aids in affordability analysis |

Key Factors Influencing Mortgage Costs

Interest Rates and Loan Terms

Interest rates and loan terms are primary drivers of mortgage costs. For example, the difference between a 15-year and a 30-year loan can be substantial, depending on individual financial situations. According to recent data, the cost of a $500,000 mortgage is roughly $3,360.16 per month over a 30-year term with a 7.1% interest rate.

For real-time insights, consider checking the interest rate in California here.

Down Payment and Loan Type

A larger down payment can significantly cut the total mortgage costs by minimizing interest and eliminating PMI. Different types of loans—such as FHA, VA, and conventional loans—each come with unique cost structures and eligibility requirements.

Additional Costs

The total mortgage cost isn’t just about principal and interest. Property taxes, homeowner’s insurance, and possible HOA fees can contribute significantly to the overall cost. Ignoring these factors might lead to unexpected financial strain.

For detailed guides, check how to handle tenants by the entirety here.

Innovative Insights on Reducing Total Mortgage Costs

Smart Refinancing

Refinancing is a strategic way to lower total mortgage costs, particularly when interest rates fall. Reviewing break-even points and potential savings can lead to substantial long-term benefits. Always look out for recent Fed decisions that impact rates directly—did the Fed raise rates today? Check here.

Early Payments and Principal Reduction

Making extra payments towards the loan principal can drastically cut down the interest paid over the life of the loan. Even modest additional contributions can yield significant savings.

Utilizing Financial Advisors

Financial advisors can help navigate the mortgage landscape, providing tailored advice according to individual financial conditions. This expert guidance can steer borrowers towards more economical choices, ensuring they get the best deals available.

Wrapping Up: Empowering Informed Decisions

In the dynamic arena of mortgage financing, total mortgage cost calculators shine as indispensable tools. They empower homeowners and potential buyers by integrating precise, comprehensive data with sophisticated calculations, supporting informed decision-making.

Homebuyers in 2024 and beyond can harness these advanced calculators to demystify the full extent of mortgage costs, paving the way for optimal financial outcomes. With the right information and tools, reaching a well-informed mortgage decision is entirely within reach. Secure a fruitful financial future by diving into the total costs—and let our simple mortgage payment calculator or The mortgage calculator assist you in making those calculations straightforward and insightful.

Fun Trivia and Interesting Facts About Total Mortgage Cost Calculators

The Birth of Mortgage Calculators

Did you know that before the creation of online mortgage calculators, many people relied on cumbersome spreadsheets and complex mathematical formulas? Thankfully, the rate calculator mortgage tools we use today have made life a lot easier! The brainchild of some innovative tech minds in the 1990s, online mortgage calculators have revolutionized the home-buying experience. This tool quickly evolved from basic interest calculations to sophisticated total mortgage cost calculators we now swear by.

Beyond Just Numbers

But what makes a total mortgage cost calculator so valuable? Well, it’s not just about crunching numbers. These calculators take into account a myriad of factors, from interest rates to taxes and private mortgage insurance. And get this; they can even adapt to the unique needs of a loan for poor credit, making homeownership more accessible to a wider audience. It’s fascinating to see how seamlessly these custom tools fit into various financial circumstances, making them indispensable for practically every borrower.

More Than Meets the Eye

Here’s a fun snippet—did you realize that using a total mortgage cost calculator can sometimes feel like getting slapped with clarity? That’s right, the stark reality it brings can be as jarring as a b-slap! While that may sound harsh, it’s actually a blessing in disguise. By laying out all the costs upfront, these calculators help you avoid nasty financial surprises down the road. This transparency makes the home-buying process more manageable, especially for first-time buyers who might feel overwhelmed.

Total mortgage cost calculators really are a game-changer, providing essential insights that can steer your financial decisions. So next time you’re pondering over mortgage options, remember these fun facts, and give your trusted calculator a whirl! You might be surprised at just how much it can offer.

How do you calculate the overall cost of a mortgage?

To figure out the overall cost of a mortgage, you’ll need to calculate the total interest you’d pay over the life of the loan plus any fees you might have. Simply divide the mortgage amount and the total interest you’d pay by the number of months you plan to repay the loan. Then, add these amounts together to get your total cost.

How do you calculate total loan cost?

To calculate the total cost of a loan, add up the total interest charges over the loan’s life and combine that with any loan fees you paid. If there were no loan fees, then the total cost is just the total interest charges you’ll pay.

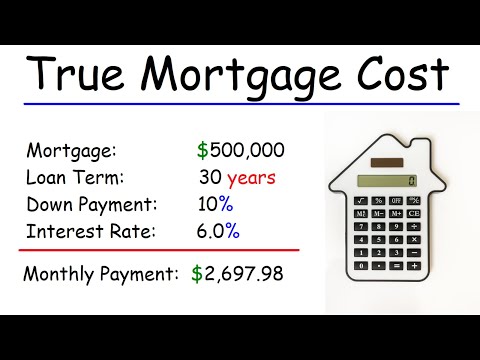

How much is a mortgage on a $500,000 house?

For a $500,000 mortgage with a 30-year term and a 7.1% interest rate, you’re looking at monthly payments of $3,360.16. Annually, this means you’ll pay $40,321.92.

How do I calculate my total mortgage loan?

To calculate your total mortgage loan, multiply the number of years in your loan term by 12 (to convert to months). For a 30-year mortgage, that’d be 360 months. Use this number to help you determine how much house you can afford by aligning it with your budget and income.

How do you calculate overall cost?

Calculating the overall cost is a straightforward deal. Just take the total interest you’d pay over the mortgage term and add any fees. If there are no fees, it’s simply the interest.

What is mortgage total cost of borrowing?

The total cost of borrowing for a mortgage is the sum of the interest you’d pay over the life of the loan plus any loan fees that might come into play, like origination fees. Without fees, it’s just the interest.

How to find the total cost of a mortgage?

To find the total cost of a mortgage, sum up all the interest you’d pay throughout the loan term and any extra fees. If there are no fees, you’re just dealing with the interest charges.

What is the formula of total cost?

The total cost formula involves adding the total interest you’d pay over the term of the loan to any loan fees you paid. Without any fees, it’s simply the total interest.

What is the real total cost of a loan?

For the real total cost of a loan, you need to tally up all the interest charges over its lifespan and tack on any loan fees that you might have paid. If there aren’t any additional fees, then it’s just the interest.

What income do you need for a $500000 mortgage?

For a $500,000 mortgage, you generally need an annual income of around $125,000 to $150,000. This can vary depending on other debts and the size of your down payment, but it’s a good ballpark figure.

What credit score do you need to buy a $500,000 house?

Buying a $500,000 house usually requires a credit score of at least 620 to 640 for most conventional loans. A higher credit score can qualify you for better interest rates and terms.

How much money do you need to put down for a $500,000 house?

Generally, you’d need to put down at least 5% to 20% for a $500,000 home. That’s anywhere from $25,000 to $100,000, which can vary based on the loan type and your lender’s requirements.

What is the formula to calculate a mortgage?

To figure out your mortgage payments, you can use the formula M = P[r(1+r)^n]/[(1+r)^n-1], where M is the monthly payment, P is the principal loan amount, r is the monthly interest rate, and n is the number of payments.

How do I calculate the total amount of my home loan?

To calculate the total amount of your home loan, you’ll need to add the total interest you’d pay over the loan term to the original loan amount. This gives you the complete picture of what you’ll owe over the years.

Will interest rates go down in 2024?

Predicting interest rates can be tricky, but some experts speculate that rates might stabilize or even slightly go down in 2024. However, it’s always wise to keep an eye on economic factors and speak to a financial advisor for precise advice.